Big Investors Are Backing Off and That’s Your Opening

BLOGAugust 5, 2026

3 min read

For years, a lot of would-be homebuyers have worried about the same thing. How do you compete with big investors who can swoop in, pay cash, and snap up the houses you want?

Well, worry a little less. Because right now, those big investors aren’t buying up the market. They’re backing out of it.

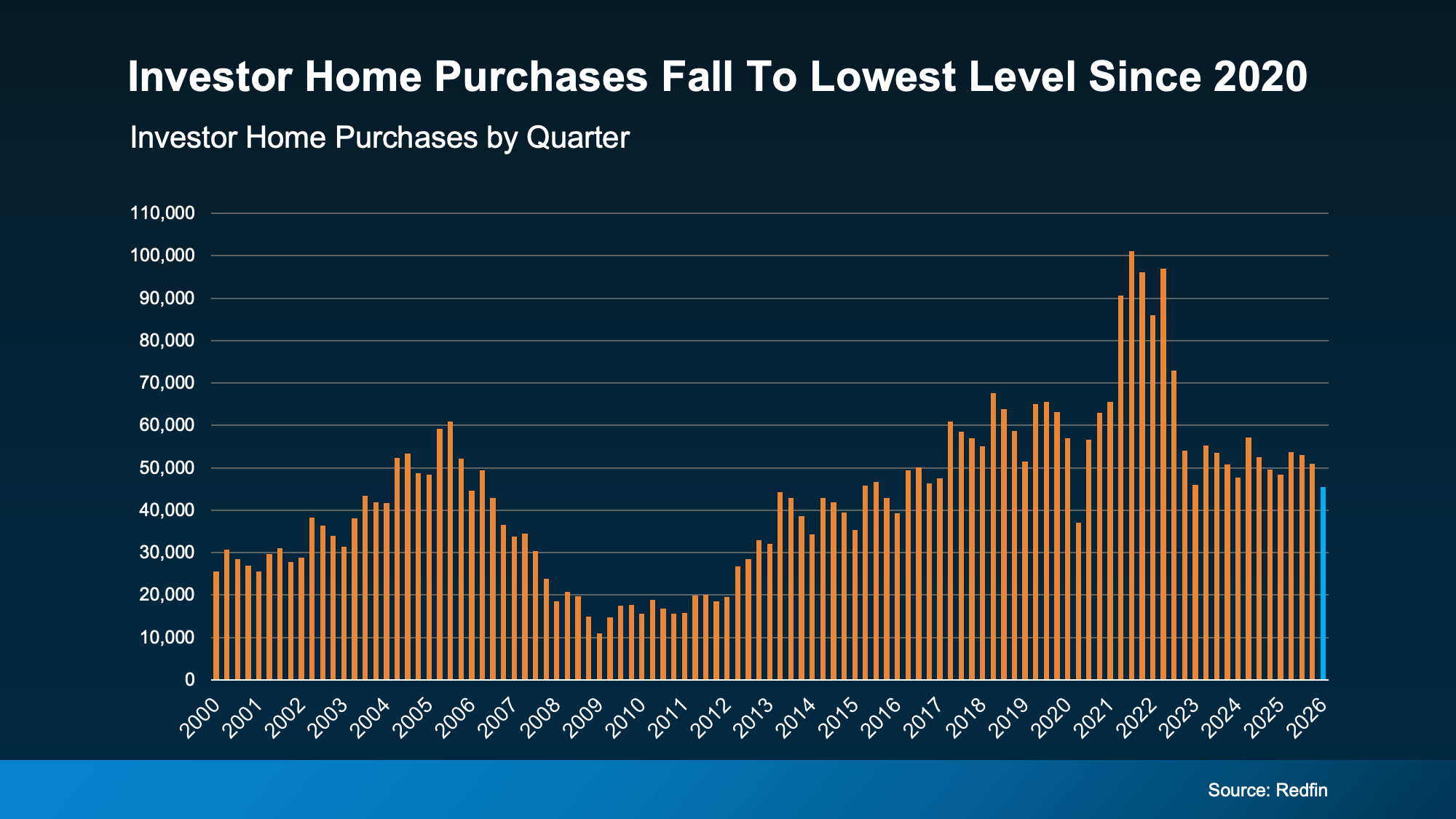

Investors Are Buying Fewer Homes Than They Have in Years

According to Redfin, investor home purchases just fell to their lowest level since 2020 – when the start of the pandemic temporarily caused pretty much all homebuying to pull way back. Before that, you’d have to go all the way back to 2016 to find a time when investors bought this few homes (see graph below):

Why the step back? Two big reasons.

First, Washington passed a housing law that takes aim at large institutional investors. To be clear, these mega investors were never as big a part of the market as the headlines made it sound. They’ve always made up a relatively small slice of housing pie. But the law still targeted the largest ones, and it worked fast. According to Thom Malone, Principal Economist at Cotality:

“When Washington announced its intention to curb institutional investors’ homebuying, the market reacted. . . Cotality data shows that investment by mega investors who own 1,000 or more properties retracted almost instantly.”

Second, the housing market has cooled. Price growth has slowed in much of the country, and in some markets, prices are dipping. That makes the math a lot less appealing for investors betting on quick gains. Lance Lambert, CEO of ResiClub, explains:

“Ever since rates spiked and the Pandemic Housing Boom fizzled out in spring 2022, institutional single-family rental (SFR) operators have pulled way back from buying up homes on the resale market—the math just isn’t as appealing right now. Home prices and rents are no longer ripping, holding costs (property taxes and insurance) have jumped, capital markets have shifted their attention elsewhere, and elevated materials prices make renovations expensive.”

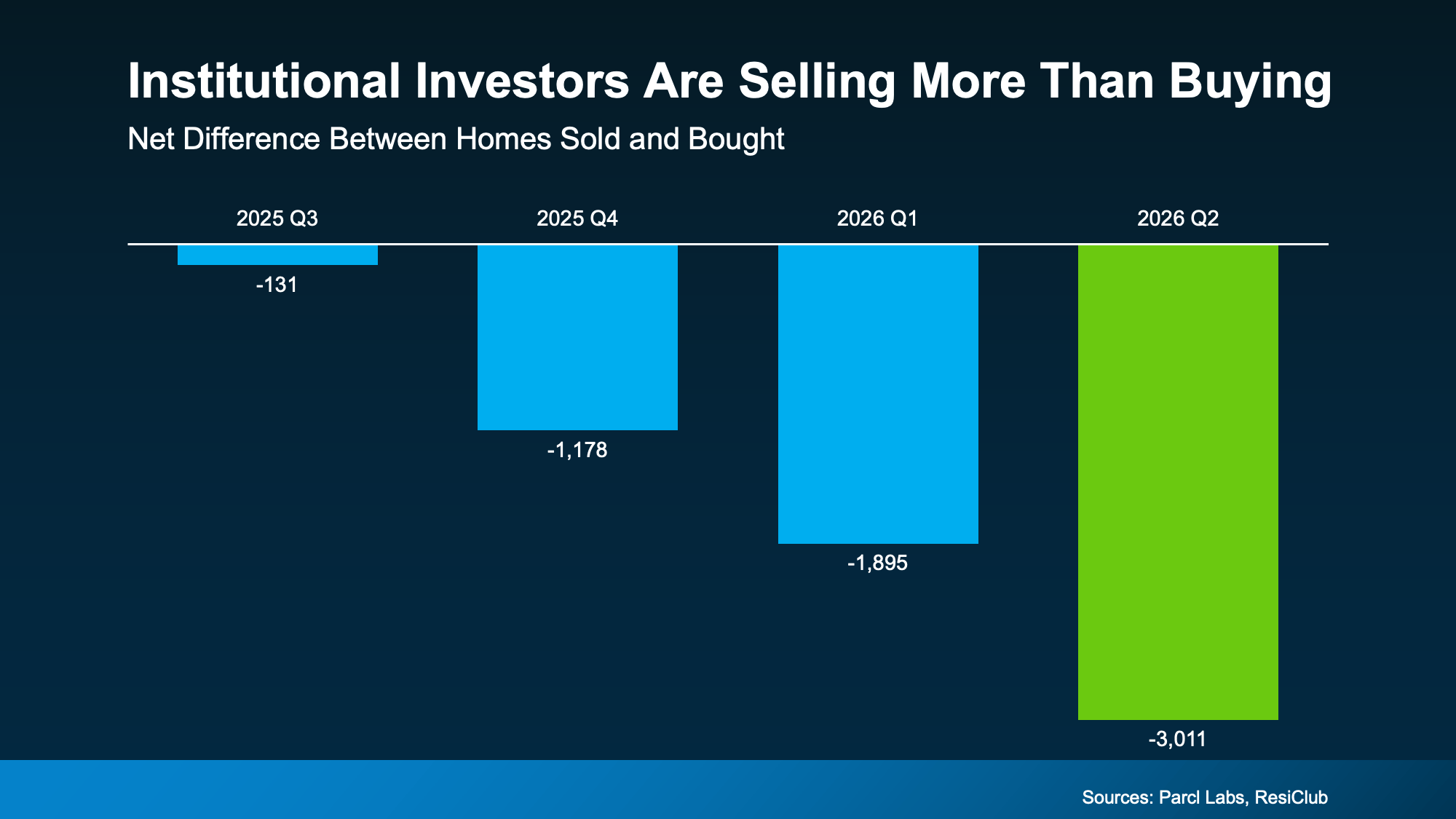

They’re Not Just Buying Less – They’re Selling More

This is the part most people miss. Big investors aren’t just slowing down their purchases. Data from Parcl Labs and ResiClub shows the largest institutional investors are now selling more homes than they’re buying – and that gap is growing these past 4 quarters (see graph below):

Every one of those homes goes right back into the market for buyers like you. And since big investors tend to own homes at the lower end of the price range, a lot of what they’re selling is exactly the kind of home first-time buyers are looking for. As Malone puts it:

“. . . this sudden dropoff in institutional investment is a signal to first-time homebuyers that there’s an opening.”

Less competition from deep-pocketed buyers. More homes hitting the market. And many of them at prices that work for a first purchase. That’s a shift that works in your favor.

Bottom Line

Big investors are stepping back, and they’re adding homes to the market as they go. If you’ve been waiting for a better shot at buying, this could be it. Let’s connect so you can see what’s popping up in our area. You may have more options than you think.