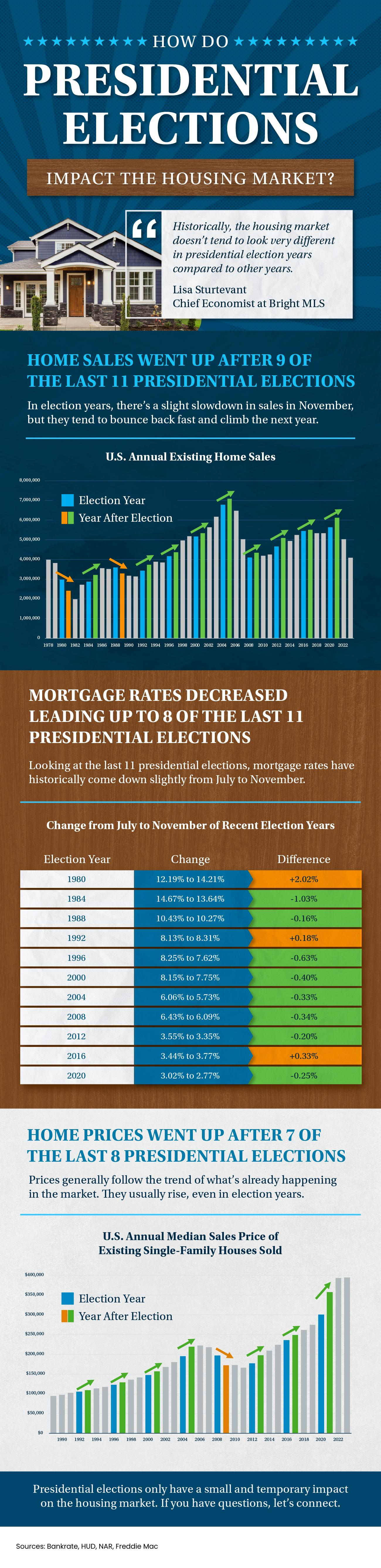

How Do Presidential Elections Impact The Housing Market

Mortgages, Refinance and Reverse Mortgages in The Villages, Florida

Helping Village Residents stay in their homes.

BLOGJuly 11, 2024

For SellersDownsizeEquitySelling Tips

2 min read

Retirement is a time for relaxation, adventure, and enjoying the things you love. As you imagine this exciting new chapter in your life, it’s important to think about whether your current home still fits your needs.

If it’s too big, too costly, or just not convenient anymore, downsizing might help you make the most of your retirement years. To find out if a smaller, more manageable home might be the perfect fit for your new lifestyle, ask yourself these questions:

If you answered yes to any of these, consider the benefits that come with downsizing.

There are many reasons why you should downsize. Here are just a few from Bankrate:

If those perks sound like something you’d want, you may already have what you need to make it happen. A recent article from Seniors Guide shares:

“And at a time when homeowners age 62 and older have more than $12 trillion in home equity, downsizing makes sense . . .”

If you’ve been in your house for a while, odds are you’re one of those homeowners who’s built up a considerable amount of equity. And that equity is something you can use to help you buy a home that better fits your needs today. Greg McBride, Chief Financial Analyst at Bankrate, explains:

“Downsizing can mean taking that equity when the home is sold and using it to pay cash or make a large down payment on a lower-priced home, reducing your monthly living expenses.”

When you’re ready to use all that equity to fuel your next move, your real estate agent will be your guide through every step of the process. That includes setting the right price for your current house when you sell, finding the home that best fits your evolving needs, and understanding what you can afford at today’s mortgage rate.

Starting your retirement journey? Think about downsizing – it could really help. When you’re ready, let’s connect.

BLOGJuly 10, 2024

For BuyersFirst-Time BuyersAgent ValueBuying Tips

3 min read

In life, patience is a virtue – but in the world of homebuying, waiting too long in hopes of finding the perfect home actually isn’t wise. That’s because the pursuit of perfection comes at a cost. And in this case, that cost may be delaying your dream of homeownership. As Bankrate explains:

“One of the most common first-time homebuyer mistakes is looking for a home that checks each of your boxes. Looking for perfection can narrow your choices and lead you to pass over good, suitable options for starter homes in the hopes that something better will come along.”

Nothing in life is ever perfect – and that’s true when you search for a home too. Unless you’re building a brand-new home from the ground up, chances are there are going to be some features or finishes you wouldn’t have picked yourself. It may be as simple as paint colors, a light fixture, or the tile in the bathrooms or kitchen. Or even that the backyard isn’t fenced in. It could also be that the home itself is great, but it’s not the ideal location you were hoping for.

But here’s the trade-off you’d be making without even realizing it. In all that time you’d spend searching for the perfect place, you’d overlook a lot of homes that would’ve worked for you. U.S. News explains:

“. . . you may miss opportunities if you enter the process with blinders on and aren’t open-minded . . . Countless potential buyers never buy because of this, and thus miss great investments or never move on to the next chapter of their lives.”

Especially with affordability and inventory where they are today, buying a home that needs some updates, is a few neighborhoods away from your ideal location, or doesn’t have all your desired features can be a smart move. Here’s why.

For starters, these homes are usually more affordable, which is important at a time when some buyers are struggling to find options in their budget.

And they give you a chance to make the space your own or discover a whole new area of town. You may find out you actually love that neighborhood. Or, swapping out a feature here or there after move-in isn’t such a big deal. So, look past the green shag carpet and see the bones of the house. With a little vision and creativity, you can turn a good house into a fantastic home.

If you’re open to a home that needs a little elbow grease or is a bit further out, let your agent know. They’ll be happy to show you how this can really open up your pool of homes to pick from. They’ll also help coach you through this process by:

1. Prioritizing Your Must-Haves: Your agent will want to revisit your wish list and separate your non-negotiables from your nice-to-haves. From there, they’ll focus on what’s really most important to you as they come up with a bigger list of options for you to choose from.

2. Coaching You To See the Potential: As you tour these added options, your agent will help you look beyond cosmetic flaws and imagine what the home could be with a little work. Simple updates like a fresh coat of paint or new flooring can make a big difference.

3. Connecting You with Local Pros: And an agent’s support goes one step further. If they know what you’re hoping to change after you move in, they can connect you with local pros who can get the job done. That way it’s less work for you, and you don’t have to worry about tracking down contractors.

Remember, there is no perfect home. But with expert help and an open mind, we can find you the right home – even in today’s market. Let’s connect to see what’s out there.

BLOGJuly 9, 2024

For SellersHome PricesSelling Tips

3 min read

If you’re thinking about selling your house, here’s something you really need to know. Even though it’s still a seller’s market today, you can’t pick just any price for your listing.

While home prices are still appreciating in most areas, they’re climbing at a slower pace because higher mortgage rates are putting a squeeze on buyer demand. At the same time, the supply of homes for sale is growing. That means buyers have more options and your house may not stand out as much, if it’s not priced right.

Those two factors combined are why the asking price you set for your house is more important today than it has been in recent years.

And some sellers are finding that out the hard way. That’s leading to more price reductions. Mike Simonsen, Founder and President of ALTOS Research, explains:

“Looking at the price reductions data set . . . It all fits in the same pattern of increasing supply and homebuyer demand that is just exhausted by high mortgage rates. . . As home sellers are faced with less demand than they expected, more of them have to reduce their prices.”

That’s because they haven’t adjusted their expectations to today’s market. Maybe they’re not working with an agent, so they don’t know what’s happening around them. Or they’re not using an agent who prioritizes being a local market expert. Either way, they aren’t basing their pricing decision on the latest data available – and that’s a miss.

If you want to avoid making a pricing mistake that could turn away buyers and delay your sale, you need to work with an agent who really knows your local market. If you lean on the right agent, they’ll help you avoid making mistakes like:

In the end, accurate pricing depends on current market conditions – and only an agent has all the data and information necessary to find the right price for your house. The right agent will use that expertise to develop a pricing strategy that’s based on current market conditions and designed to get your house sold. That way you don’t miss the mark.

The right asking price is even more important today than it’s been over the last few years. To avoid making a costly mistake, let’s work together.

BLOGJuly 8, 2024

4 min read

Even if you didn’t own a home at the time, you probably remember the housing crisis in 2008. That crash impacted the lives of countless people, and many now live with the worry that something like that could happen again. But rest easy, because things are different than they were back then. As Business Insider says:

“Though many Americans believe the housing market is at risk of crashing, the economists who study housing market conditions overwhelmingly do not expect a crash in 2024 or beyond.”

Here’s why experts are so confident. For the market (and home prices) to crash, there would have to be too many houses for sale, but the data doesn’t show that’s happening. Right now, there’s an undersupply, not an oversupply like the last time – and that’s true even with the inventory growth we’ve seen this year. You see, the housing supply comes from three main sources:

And if we look at those three main sources of inventory, you’ll see it’s clear this isn’t like 2008.

Although the supply of existing (previously owned) homes is up compared to this time last year, it’s still low overall. And while this varies by local market, nationally, the current months’ supply is well below the norm, and even further below what we saw during the crash. The graph below shows this more clearly.

If you look at the latest data (shown in green), compared to 2008 (shown in red), we only have about a third of that available inventory today.

So, what does this mean? There just aren’t enough homes available to make values drop. To have a repeat of 2008, there’d need to be a lot more people selling their houses with very few buyers, and that’s not the case right now.

People are also talking a lot about what’s going on with newly built houses these days, and that might make you wonder if homebuilders are overdoing it. Even though new homes make up a larger percentage of the total inventory than the norm, there’s no need for alarm. Here’s why.

The graph below uses data from the Census to show the number of new houses built over the last 52 years. The orange on the graph shows the overbuilding that happened in the lead-up to the crash. And, if you look at the red in the graph, you’ll see that builders have been underbuilding pretty consistently since then:

There’s just too much of a gap to make up. Builders aren’t overbuilding today, they’re catching up. A recent article from Bankrate says:

“What’s more, builders remember the Great Recession all too well, and they’ve been cautious about their pace of construction. The result is an ongoing shortage of homes for sale.”

The last place inventory can come from is distressed properties, including short sales and foreclosures. During the housing crisis, there was a flood of foreclosures due to lending standards that allowed many people to get a home loan they couldn’t truly afford.

Today, lending standards are much tighter, resulting in more qualified buyers and far fewer foreclosures. The graph below uses data from ATTOM to show how things have changed since the housing crash:

This graph makes it clear that as lending standards got tighter and buyers became more qualified, the number of foreclosures started to go down. And in 2020 and 2021, the combination of a moratorium on foreclosures (shown in black) and the forbearance program helped prevent a repeat of the wave of foreclosures we saw when the market crashed.

While you may see headlines that foreclosure volume is ticking up – remember, that’s only compared to recent years when very few foreclosures happened. We’re still below the normal level we’d see in a typical year.

Inventory levels aren’t anywhere near where they’d need to be for prices to drop significantly and the housing market to crash. As Forbes explains:

“As already-high home prices continue trending upward, you may be concerned that we’re in a bubble ready to pop. However, the likelihood of a housing market crash—a rapid drop in unsustainably high home prices due to waning demand—remains low for 2024.”

Mark Fleming, Chief Economist at First American, points to the laws of supply and demand as a reason why we aren’t headed for a crash:

“There’s just generally not enough supply. There are more people than housing inventory. It’s Econ 101.”

And Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“We will not have a repeat of the 2008–2012 housing market crash. There are no risky subprime mortgages that could implode, nor the combination of a massive oversupply and overproduction of homes.”

The market doesn’t have enough available homes for a repeat of the 2008 housing crisis – and there’s nothing that suggests that will change anytime soon. That’s why housing experts and inventory data tell us there isn’t a crash on the horizon.

BLOGJuly 4, 2024

2 min read

Everyone’s vision for the future is personal and unique. But for many, common goals include success, freedom, and prosperity — values closely tied to having your own home and the iconic feeling of achieving the American Dream.

A recent survey by Bankrate reveals exactly that: homeownership is still a part of the American Dream. The results show, at 78%, that owning a home tops the list, surpassing other significant milestones such as retirement, having a successful career, and more (see below):

So, why is buying a home important to so many today? One reason is the financial and physical security it provides. Many people see homeownership as a way to reduce stress because owning a home with a fixed-rate mortgage stabilizes what is likely their largest monthly expense.

Another factor is the potential for building wealth. That’s because, over time, homeowners gain equity as they pay down their mortgage and as home prices appreciate, leading to longer-term financial stability.

But what about the responsibilities that come with owning and maintaining a home? According to a survey by Entrata, only 23% of renters feel homeownership is too much work, indicating the majority are open to the commitments and obligations that come with being a homeowner.

While buying a home today might seem daunting due to higher mortgage rates and rising home prices, the long-term benefits can make it worthwhile. If you’re considering homeownership, remember that it’s more than just a financial investment — it’s a step toward securing your future.

Owning a home is a significant and powerful decision that represents a big part of the American Dream. If you’re ready to take this step, let’s connect so you have someone who can guide you through the process and help you make your homeownership goals a reality.

BLOGJuly 3, 2024

2 min read

If you own a home, your net worth has probably gone up a lot over the past year. Home prices have been rising, which means you’re building equity much faster than you might think. Here’s how it works.

Equity is the current value of your home minus what you owe on the loan.

Over the past year, there have still been more people wanting to buy than there are homes available for sale, and that’s pushed prices up. That rise in prices has translated directly into increasing equity for homeowners.

According to the latest Homeowner Equity Insights from CoreLogic, the average homeowner’s equity has grown by $28,000 in the last year alone.

That’s the national average, so if you want to see what’s happening in your state, check out the map below. It uses data from CoreLogic to show how much equity has grown in each state over the past year. You’ll notice every single state with sufficient data saw annual equity gains:

If you bought your house before the pandemic, the equity news is even better. According to data from Realtor.com, home prices shot up by 37.5% from May 2019 to May 2024, meaning your home’s value has likely increased significantly. Ralph McLaughlin, Senior Economist at Realtor.com, says:

“Homeowners have seen extraordinary gains in home equity over the past five years.”

To give context to how much equity can stack up over time, Selma Hepp, Chief Economist at CoreLogic, explains the total equity the typical homeowner has today:

“With home prices continuing to reach new highs, owners are also seeing their equity approach the historic peaks of 2023, close to a total of $305,000 per owner.”

With how prices skyrocketed a few years ago, and the ongoing price growth today, homeowners clearly have substantial equity built up – and that has some serious benefits.

You could use it to start a business, fund an education, or even to help you afford your next home. When you sell, the equity you’ve built up comes back to you, and may be enough to cover a big part – or even all – of your next home’s down payment.

If you’re planning to move, the equity you’ve gained can really help. Curious about how much you have and how you can use it to help pay for your next home? Let’s connect.

BLOGJuly 2, 2024

For BuyersHome PricesMortgage RatesBuying Tips

2 min read

With all the headlines circulating about home prices and mortgage rates, you may be asking yourself if it still makes sense to buy a home right now, or if it’s better to keep renting. Here’s some information that could help put your mind at ease by showing that investing in a home is still a powerful decision.

According to the experts at Gallup, real estate has been crowned the top long-term investment for a whopping 12 years in a row. It has consistently beat out other investment types like gold, stocks, and bonds. Just take a look at the graph below – it speaks volumes:

But why does real estate continue to reign supreme as a top-notch long-term investment? It’s because, even today, buying a home can be your golden ticket to building wealth over time.

Unlike other investments that can feel a bit like riding a rollercoaster with all the ups and downs and ongoing risk factors, real estate follows a more predictable and positive pattern.

History shows home values usually rise. And while prices may vary by market, that means as time goes by, your house is likely to appreciate in value. And that helps you grow your net worth in a big way. As an article from Realtor.com explains:

“Homeownership has long been tied to building wealth—and for good reason. Instead of throwing rent money out the window each month, owning a home allows you to build home equity. And over time, equity can turn your mortgage debt into a sizeable asset.”

So, if you’re on the fence about whether to rent or buy, remember that real estate was consistently voted the best long-term investment for a reason. And if you want to get in on that action, it may make sense to go ahead and buy (if you’re ready and able).

When it comes to building wealth that stands the test of time, real estate is the name of the game. If you’re ready to start on your own journey toward homeownership, let’s connect today.

BLOGJuly 1, 2024

3 min read

If your listing expired and your house didn’t sell, it’s totally natural to feel a mix of frustration and disappointment. And as you’re working through that, you’re probably also wondering what went wrong and what you should do next.

If you still need to move and want to get it back on the market, here are some things to consider as you look back.

Setting the right price from the start is key. While it might be tempting to try shooting high with your price, that can slow down the selling process big time. If your house was priced higher than others similar to it, it may have turned away buyers. And that’s likely why it sat on the market. As Rocket Mortgage explains:

“Buyer interest in your home is highest when it first comes on the market. That’s why it’s so important to start with the right price on day one. . . If you overprice your house, buyers may just raise an eyebrow and move on to the next listing without even coming for a showing. . . It can be easy to think your home is worth more but try not to let sentimental value color your judgment. Your home’s true value is whatever a buyer is willing to pay for it.”

One of the biggest mistakes you can make when selling your house is overly restricting the days and times when potential buyers can tour it. Even though it might feel stressful to drop everything and leave when buyers want to see your house, being flexible with your schedule is important. After all, minimal access means minimal exposure to buyers. ShowingTime advises:

“. . . do your best to be as flexible as possible when granting access to your house for showings.”

If buyers weren’t interested in your house, it’s worth taking another look at your home through their eyes. Are there outstanding repairs that may be distracting them? Even if it’s a small thing, some buyers may see it as a sign the maintenance on the home is falling behind.

Just remember, you don’t always need to make big upgrades. Selective small repairs or touch-ups go a long way. Things like tidying up your landscaping, a fresh coat of paint inside, or removing personal items and clutter can work wonders in sprucing up the house for potential buyers. You could also consider staging the home.

If there were offers coming in, but you weren’t ready to negotiate, that may be another reason why it didn’t sell. While you want to get top dollar for your house, you also need to be realistic about what your house can net in today’s market. The market is still tipped in a seller’s favor, but the supply of homes for sale is growing and buyers are feeling the sting of higher mortgage rates. So being willing to play ball can make closing a deal a whole lot easier. A skilled agent can help. As Ramsey Solutions explains:

“If you don’t have the money or time to fix home issues, consider offering some other form of incentive to buyers. . . An experienced real estate agent can help you arrange a deal where you and your buyer both come out on top.”

If you want an expert’s advice on why it didn’t sell, rely on a trusted real estate agent. Whether that’s the agent you used previously or a new one once the listing has officially expired, a great agent will sit down and take the time to talk it over with you. They’ll want to hear your honest opinion on what worked and what didn’t, and where you want to go from here.

Then, they’ll offer their perspective. This includes tailored advice and effective strategies for re-listing your house to get it sold. As Better Homes & Gardens says, an agent should be your go-to resource in this situation:

“If you’re frustrated with the timeline of your sale, chat with your real estate agent. Agents want what is best for you and the sale of your home, and having open communication about any frustrations will be key.”

It’s natural to feel disappointed when your listing has expired and your house didn’t sell. Connect with a reliable real estate agent to determine what happened, and what changes you should make to get your house back on the market.